GOLD: Is it really pricing the real value of the asset

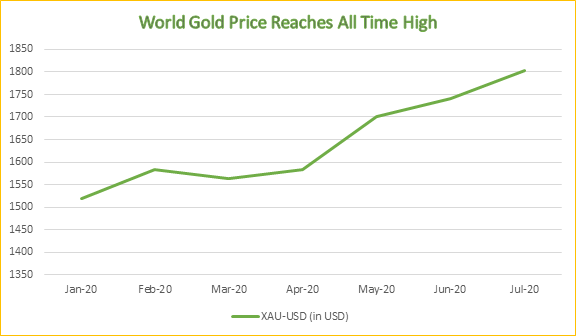

Gold started CY 2020 at USD 1520 and has reached USD 1945 on 30 July 2020. That’s a gain of 28 % in 7 months , annualised at 48 %.

The lower interest rates , Central bank stimulus and the pandemic have helped this asset class push to prices not seen since 2011.

But two important events have coincided with Gold prices in 2020.

As the pandemic rattled markets in late-March, gold too suffered a sell-off as investors rushed to free up cash.

Since then, however, buyers have returned to gold, seeing it as a safe store for their money

If Gold is supposed to be Safe Haven , then how is Equities doing so well along with Gold ?

There are few ways to buy Gold

Buy physical

Buy ETFs

Though there are other alternatives to buy Gold , but typically it’s physical and ETF which are preferred methods to park cash in Gold assets as Safe Haven class.

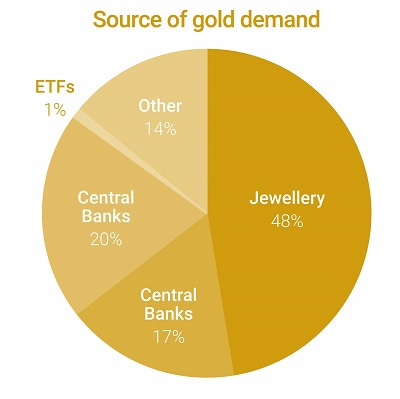

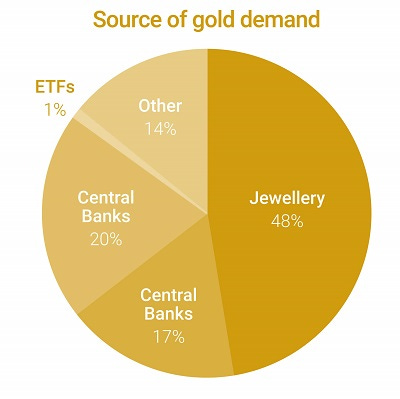

During Q1 of 2020 , Physical demand for gold – consisting of jewelry, industrial uses, central-bank purchases and retail buying of bars and coins – fell by 26% year-on-year to 753 metric tons in the first quarter, the lowest level since 2009, as high prices led to the drop in consumption.

China’s jewelry-fabrication demand also tumbled 62% due to the COVID-19 pandemic, which shut down the economy,

India’s fabrication demand fell 34% from the same period a year ago, hurt by record high gold prices in the country’s currency even before a government-mandated lockdown in late March

First-quarter demand for gold used in industrial applications fell 19% to 75 tons

Coin and bar retail investment fell by 11% year-on-year in the first quarter to 240 tons, led by a 21% drop in physical bar investment to 151 tons,

Demand in Asia fell by 67% in Q1 compared to prior year.

Demand in China and India for physical bars fell by 53% and 49%, respectively, hurt by an economic slowdown, high gold prices and a lockdown in China, which brought business activity and consumption to a standstill.

Demand in Western nations, however, as a surge for safe-haven meant more than doubled in Europe and was up 21% in North America during Q1.

Gold-linked exchange-traded products are growing in popularity with investors , Gold ETFs closed H1 with record US$40bn of net inflows.

But do all these Gold ETF’s actually hold physical metal sufficient to back their market capitalizations on a 1:1 basis. Some of them very well might; others almost certainly don’t.

Many of these gold instruments hold futures contracts and other financial derivative products that merely “track” the gold price.

The biggest of them all – SPDR Gold Shares (NYSE:GLD) – purports to have 100% backing of its $78 billion market capitalization in physical bullion. But it’s practically impossible to achieve around the clock since the fund’s assets are a moving target. As an open-ended fund, SPDR Gold Shares doesn’t hold a fixed quantity of gold. A close inspection of its prospectus reveals that it relies on layers of financial intermediaries to create shares and manage its gold inflows and outflows.

That creates a tremendous amount of counterparty risk, including the risk that some of the gold claimed in vaults by SPDR Gold Shares may be rehypothecated, or simultaneously owned by another party. Rehypothecation is defined by Investopedia as “the practice by banks and brokers of using, for their own purposes, assets that have been posted as collateral by their clients.”

Banking and gold don’t go well together – not for gold investors, anyway. The whole point of owning a hard asset is to have wealth outside of the financial system!

It’s easier for billionaires and institutional investors such as hedge funds to move millions of dollars into gold via an ETF rather than through the purchase of gold coins. Some “smart money” may be moving into gold via this route.

Owning gold indirectly through financial instruments obviously isn’t the smartest strategy for obtaining true diversification out of financial assets. But people who have made fortunes in financial markets tend to perceive it as the only game in town.

The opportunity is that tens of billions of dollars parked in gold and silver derivatives meant to represent precious metals may create something of a force majeure on one or more of the bullion banks – or the futures market itself. If one link in the system fails or is exposed as fraudulent, then confidence could collapse in all forms of paper gold.

Paper/IOU gold may be “convenient” but it is inherently untrustworthy as compared to the real thing.

Credits: Stefan Gleason , Allen Sykora , Karen Gilchrist , Refinitiv Metal Research.